The Big Reset for Corporate Venture Building - Long live Investment Building!

Authors: Misha de Sterke, Jeroen Tjepkema

Part a: Corporate innovation redefined

“A conspicuous failure.” “Hardly more than a toy.” “A development of which we need waste little time dreaming.” It may seem unbelievable now, but these were the initial reactions to the electric light bulb, the telephone, and the television - some of the most widely used, world-changing innovations ever seen. Innovation may be attacked, criticized, or even ridiculed - but no business can afford to view it as unimportant. However, for innovation to be pursued effectively, it must first be properly defined to make sense within the corporate environment.

Ill-defined corporate innovation and growth initiatives have led to the opening and closing of many innovation labs. Annually, $2.4 trillion is spent on R&D on a global level, despite the fact that between 80 and 90% of product launches in the CPG industry fail. To put this in perspective, consider that the top 50 CPG companies account for nearly 60% of global industry sales - yet they capture a mere 2% of its growth. The time is right to redefine corporate innovation to help large companies capture growth faster, more efficiently and in a more consumer-centric manner.

A renewed definition

Corporate innovation =

A strategic method that avoids small, niche ideas in favor of expanding and adapting existing products/services in new ways to improve and grow the core business. The goal is to develop a growth portfolio that bridges a company's growth gap, future-proofs revenue streams and creates a compelling growth story for investors. It’s about protecting, growing or transforming the core - not moving away from it.

This re-evaluation of what corporate innovation means is especially necessary for some of the world’s largest companies, where existing processes are not equipped to leverage core assets in exploring new business models

Instead of supporting entrepreneurs to adapt to any hurdle that enters their path, the opposite approach is often favored by corporations, relying on organizational charts and rigid procedures to provide structure for renovating their product portfolios to align with near-future consumer demand. For most, this simply creates the least tension with existing processes and allows corporations to maintain size. However, at the same time, it also introduces inertia, preventing the corporation from operating differently.

The corporation’s scale usually determines its capability of adapting portfolios to fit broader sociocultural trends, such as urbanization, demographic shifts, or recruitment needs. For corporations, this fuels the need for an M&A to register a quick win, but this is an expensive approach and, according to Harvard Business Review, the failure rate for all mergers and acquisitions is between 70 and 90%.

Timing is everything

With a focus on near-term innovation to protect their existing size, margins and market share, corporations have trouble understanding the impact of long-term trends on their product portfolios. If corporates embrace a trend too early, innovations remain too small to compete internally with existing product portfolios for funding, while stepping in too late means they enter a deep shade of red ocean. It’s about balance, weighing up innovation and execution to create. In Rita McGrath’s words, it’s about creating “an imagination premium that Wall Street can get behind”.

This imagination premium (McGrath, 2021) describes the value of a company's equity beyond what can be readily explained by its current reality. It’s why companies like Amazon and Tesla derive huge valuations based on investors’ belief in their potential growth and market share potential.

Why is this important?

Any indecision around future-proofing your existing product portfolio devalues the imagination premium as it allows for the rapid growth of relatively young players or for competitors to pick up early market share. Examples include AB InBev with its eB2B platform BEES, which is leading the way with over 31 million users. Or Ellure, the Swedish cosmetics brand that combines the Internet of Things and 3D printing to allow shoppers to create personalized custom liquid lipsticks online.

When visualized, the imagination premium shows another, underlying, effect - the growth gap. At some point in time, a product or portfolio of products will be set for decline in an unaltered state, creating space for competition and inviting challengers to eat up market share. Innovation is therefore essential for any business to both sustain its current market share and to expand it. Where the growth gap describes the revenue demand for product innovation and shows the gap between what the core business can deliver now versus what it needs to deliver to create shareholder value, the imagination premium describes the potential for category growth. Both views are essential for a future outlook

When we plot innovation horizons (Baghai, Coley & White, 2000) it becomes clear that near-future innovations will push for the sustainability of current growth while mid-to-long-term growth will push for business model extension. This also shows clearly why the premise of corporate incubators pursuing business model innovation largely fails. Future growth is needed in the short term to fill the growth gap but the benefits of incubators are too fragile to survive among the big numbers.

Our renewed call for core innovation is about putting a clear process in place to include product innovation within product portfolio development. It’s not about growing a new business from scratch but rather, if the opportunity is big and impactful enough, acquiring or creating access to certain assets that allows you to push existing brands into new spaces and expand category growth. Your future portfolio omission becomes the core.

Out with the old

For a corporation, simply applying Lean Startup methodologies is no longer sufficient and creating complicated, highly theoretical models to solve the ‘scaling up’ challenge will not work in practice. The challenge for any corporate innovator will shift from building MVPs to understanding what the financial thresholds are that determine whether innovation can plug the growth gap. Innovations should be looked at as investments. Create value, demonstrate the growth trajectory and then “sell” that innovation back to the mothership for core growth.

It is time for a big reset in corporate venture building land!

Chapter summary: Innovation redefined:

Part b: The corporate innovation contradiction

It’s understandable if you’ve come to view “corporate innovation” as a contradiction in terms. As we know from Steve Blank, the operating model of large corporations focuses on execution at a large scale. With incubators, it’s here that things start to go wrong as corporate innovators and venture builders alike often try to create something that requires too much change from the mothership in order to work. They may have found a consumer pain point but did not take into account the feasibility nor, in most cases, the viability requirements to scale the MVP internally and compete against a set of resource/investment priorities within the core business. The confusion can be that people blame it on politics but from our experience, venture teams do not know their internal customers well enough.

Recognizing this contradiction is nothing new, of course. Clayton Christensen’s The Innovator's Dilemma described how large incumbent corporates can lose market share to unexpected, fast-rising rivals back in 1997.

We identify three main arguments that prevent corporate venture building from succeeding in its current state:

If these investor concerns resonate, it’s because the company has either not done a good job of communicating the value of its growth investments, or investors simply don't believe what they are being told.

Breaking through, not breaking away

Corporates’ inability to successfully re-invent themselves is not for the want of trying. More often than not, corporates launch accelerator programs to innovate themselves or partner with more agile startups. But the dominant narrative most innovation agencies and corporate venture builders tell incumbents is that they should change an old company like Unilever into a digital native one like Amazon that is consumer-obsessed and breaks things while they are executing. We think that is an unrealistic fantasy. Most executives do not want to take such risks, and poor innovation success rates prove them right.

We see the likes of ABinBev’s pitstop innovation, a low-cost retail channel focussing on ‘impulse’ occasions for cold beers, as a great example of an innovation that delivers significant growth, builds upon the core assets of the business, and breaks market entry barriers. When it comes to breakthrough innovation, it is important to have executed your own due diligence around consumer pains and benefits first, discovering the right time to execute. Then it’s about building or scouting for new companies that fit these buckets, running ‘proof of concepts’, testing the core brand’s potential fit and making (small) investments.

The major shift in thinking is that corporate innovation needs to be an operational instrument embedded within the business itself - one that drives growth in the core or makes things that become the new core. This means corporate venture building teams should explore and bring home the results. The core business owns the acquisitions and scaling-up pathway. This also means that core business leaders need to be incentivized to take ownership of the business not only in the short term but also in the long term.

Incubators, the worst of all possible worlds?

It’s an unfortunate fact that many ventures fall flat before taking off - even when outside support is sought. For instance, research by the University of Cambridge found that incubators typically have a life cycle of three to five years. The same research shows that seeking value by taking equity in startup-scaleups, mostly results in delays in revenue generation that sees the same incubators prioritizing short-term profit over long-term performance.

Unilever’s own in-house incubator, The Uncovery, which was shut down in October 2023, is a case in point. In the words of Andrew Ross, senior advisor and venture partner at XRC Ventures, “The solution to create something ‘outside’ the regular system, but still within the corporation makes sense at least on paper. [But] we think experience has shown that, in many cases, you end up with the worst of all possible worlds.” This challenge is described in Tuschman and O'Reilly’s (2004) concept of ambidexterity, a concept that in reality is only viable for the few. To pull this off, corporate innovation leaders need to be highly skilled in building ties and bridges with key stakeholders at the mothership and dealing with conflicts of interest around agenda setting, different ambitions, the ‘not invented here’ syndrome and many more challenges. Managing the underlying tensions in corporate stakeholder management is an art and requires almost ‘Freudian’ capabilities.

The closure of The Uncovery and many other innovation labs in the last few years, including at Migros, one of the largest retailers in Europe, suggests Ross is right. That’s certainly our view, with many labs producing innovations that are too small, require too much change, or are too niche to survive in a corporate environment. Instead, investments related to the core, competing for the same budget, kill them off. And even when a potential innovation looks promising, which senior executive would like to take that bold decision?

The common theme with internal innovations is that forecasting is unclear regarding profitability. Since most innovation teams are not investment managers and thus do not define the financial thresholds for the business to invest further, teams are unable to forecast their funding trajectories. Corporates remain mired in the status quo. There is no sanity in trying to force-fit the perspective of a venture builder to the machine of the corporation.

So if everybody is doing it, but nobody really succeeds, what’s next? Corporate venture building is dead - Long live Investment building!

Chapter summary: The corporate innovation contradiction

Part c: A reset of corporate venture building

“We were right about some things and overconfident concerning others.”

When we started with corporate innovation and venture building in 2015, we worked on every type of project you can imagine for the largest companies in the world. In all those years, we created value for companies on top of the growth we delivered. We were part of cultural change programs, trained support functions in how to enable innovation, visited multiple boardrooms to discuss incubation setups, and delivered keynotes all over the world.

The learnings from these early stages of venture building were captured in the book “The 10x Growth Machine,” (2020). The book called for a better net-sales contribution from innovation and defined a set of pillars to help corporations scale innovations more successfully or stop them earlier in the process.

But learning never stops. Where we used to frame corporate innovation as a methodology to break away from the corporate mold, best executed in accelerators and incubators, we have now come to the conclusion that corporate innovation needs to be an operational instrument embedded within the company itself - one that drives growth in the core or makes things that become the new core.

The most important lesson however is not to underestimate the power of venture building. This can, in fact, be a hugely impactful way of driving innovation at corporates, but it is often applied incorrectly.

Venture building should be about rapid exploration, but the ultimate mission for intrapreneurs should be to bring results back to the mothership. There are corporations that do this well, with PepsiCo being a good example. Despite being one of the largest food and beverage companies in the world, it boasts a strong innovation pipeline. In part, this is due to the way its innovation arm, PepsiCo Labs, collaborates with cutting-edge startups and investors to implement innovations back within the core. This is a great alternative for de-risking R&D investments.

Unfortunately, platforms and structures are often reorganized but rarely invest in increasing maturity because of high levels of uncertainty (Chesbrough, 2019). The idea that R&D innovation needs to be ‘in control’ of the organization is a paradigm from the past. The same will become true of venture building if things don’t change. With the number of corporates where innovations have not provided the desired results increasing, venture building will be labeled as an unsuccessful concept for any corporate and become extinct as a methodology.

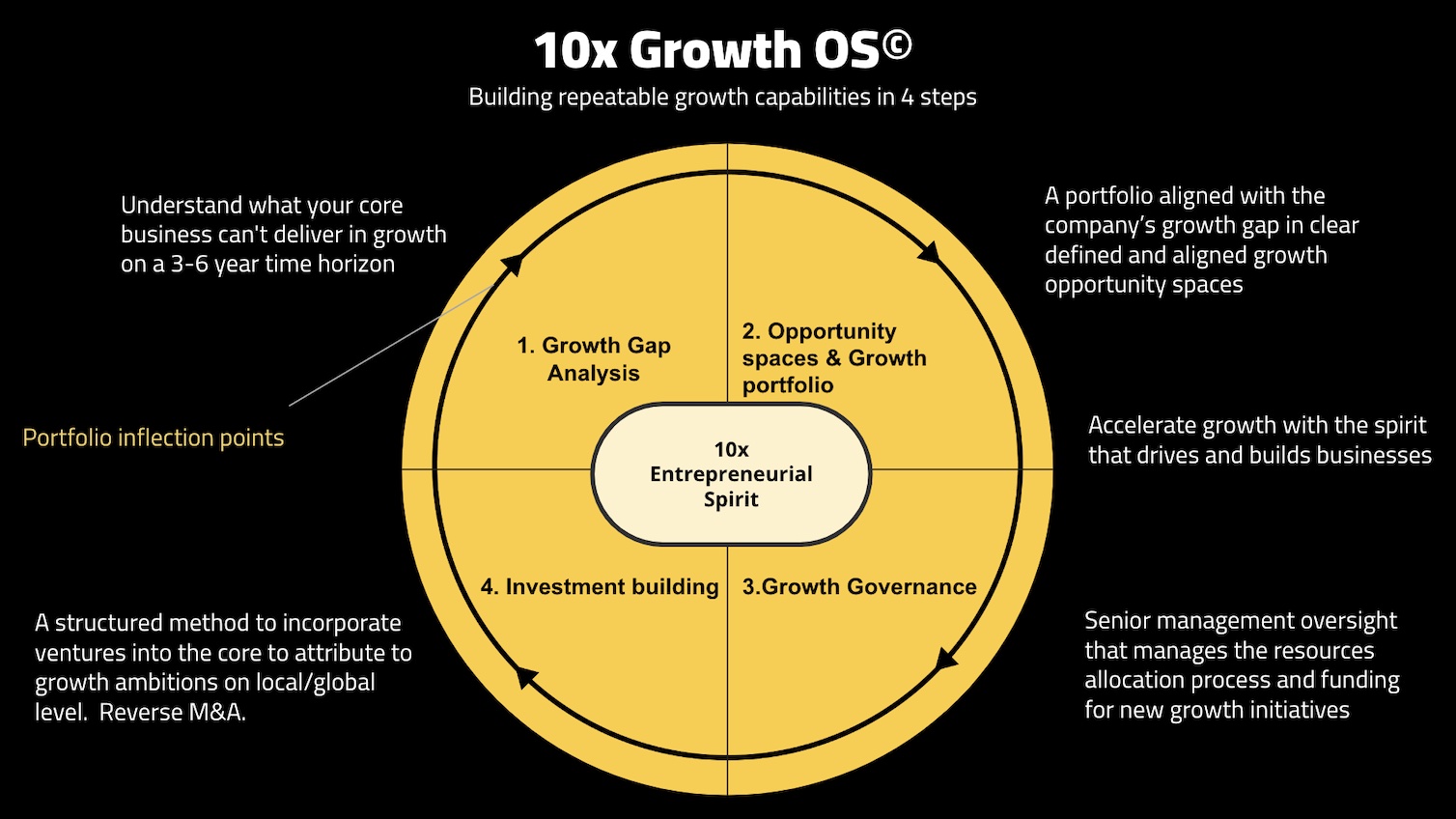

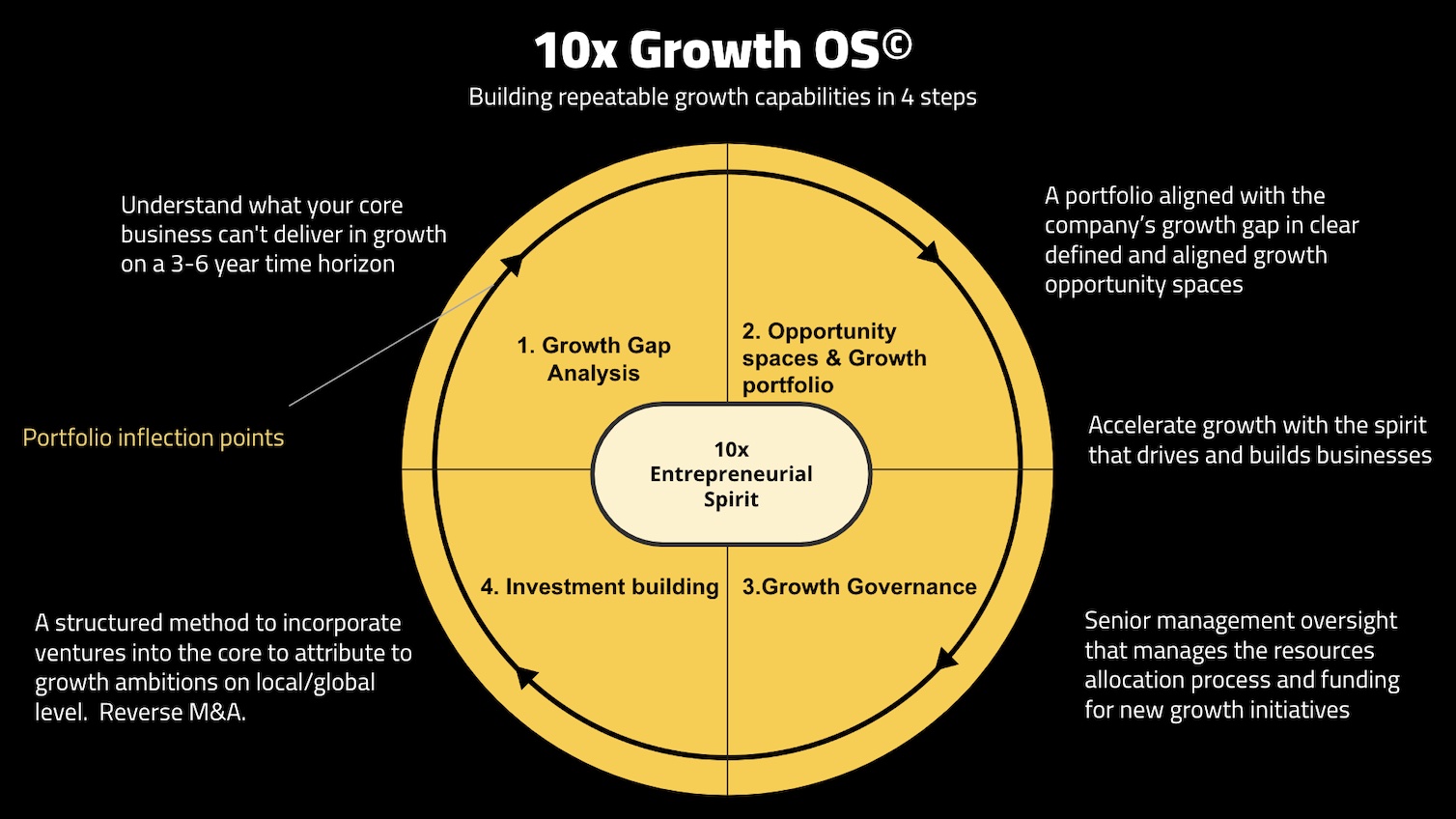

Introducing our renewed 10x Operating System ⓒ

“We have learned precisely what a corporation can and should do, as well as what they fantasize about and should not do.”

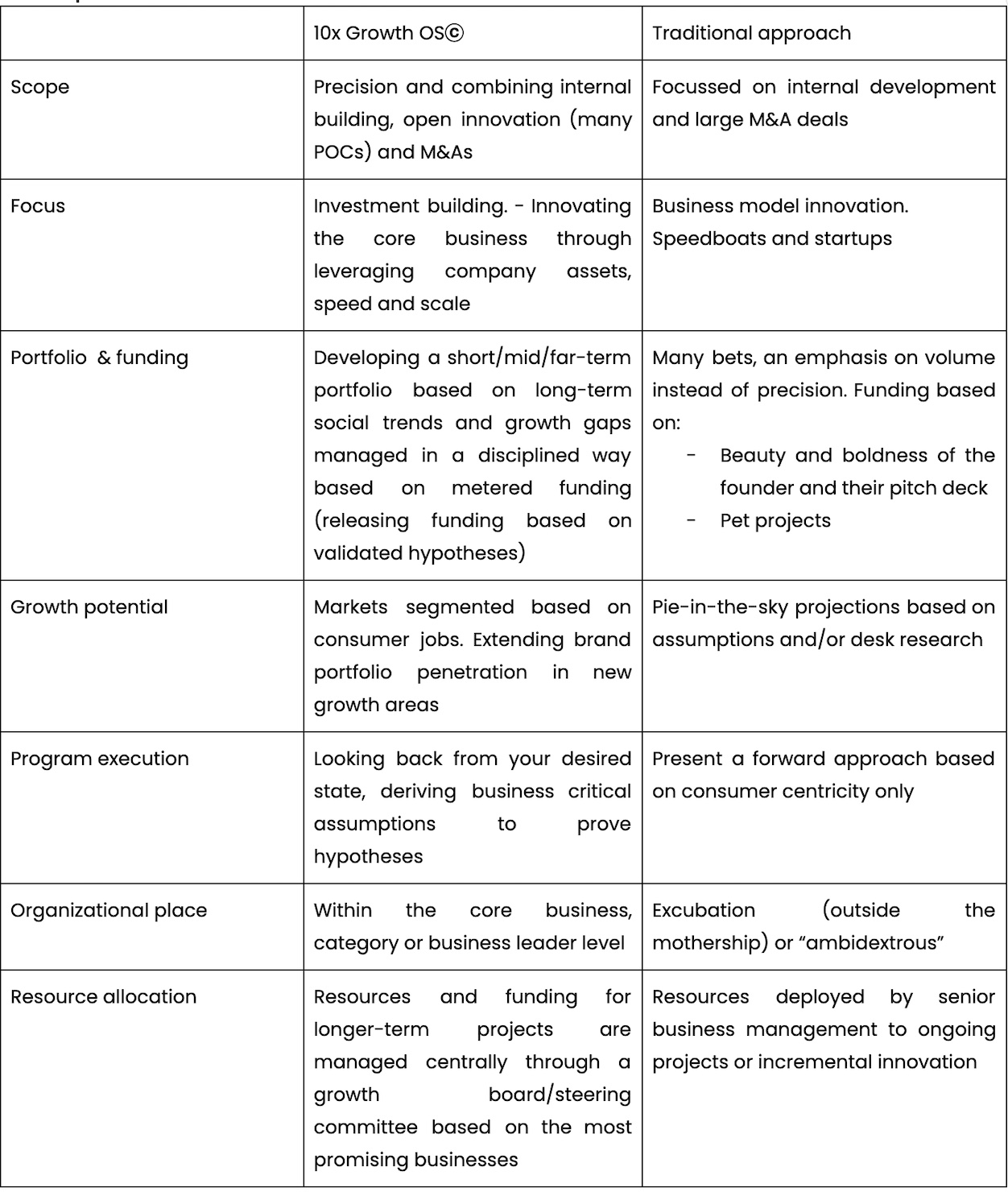

We observed that corporate venture building and incubators focussed on innovation that stretched beyond the core (while not leveraging core assets). This was, in a sense, futuristic. This was partly because that was what corporations (thought they) wanted or needed. With the 10x Growth OS we present a reset in mindset, accountability and execution - leveling up from the venture-building approach as we know it to an innovation approach focussed on core growth:

The 10x Operating Systemⓒ is about adopting a holistic approach to growth by combining an investment ethos with a venture-building methodology. Applying this will create a tactical bridge between strategy and execution. With so many moving pieces in the puzzle, it is only possible to know if your innovation strategy is working by creating holistic oversight. If there are gaps in your field of vision, perhaps because the market conditions have changed, and you still adopt the same approach, your innovation strategy is likely to fail. It lacks precision. And that’s the kind of uncertainty we can avoid.

Adopting the 10xGrowth process and the building blocks involved will help you answer the fundamental questions when driving successful corporate innovation (programs).

When visualized, the 10x Growth OS contains four building blocks that, when applied properly, will create a flywheel for core growth innovation. Let’s deep dive into each building block.

Step 1: The Growth Gap: The north star of your growth portfolio

In order to develop an impactful growth portfolio to protect, grow and/or transform the core you need to have a clear understanding of what your company’s ‘growth gap’ is (Anthony, 2020). The growth gap is determined by the difference between your growth aspiration at any point in time and what your core and adjacent businesses can deliver in the future. This number will become your north star and a benchmark to size your portfolio, including how many initiatives, varying from geographic expansion to new product innovation, you must pursue to reach this number in the future. As a result, the innovation portfolio encompasses short-, mid- and long-term initiatives that protect, grow or transform the core.

The growth gap estimation will be used as your line in the sand to answer the following questions:

As market conditions change continuously, whether due to sociocultural trends or competitors launching the exact same idea, the growth gap analysis requires frequent “maintenance”. A continuous loop is necessary to achieve timely competitive advantages. In this sense, your growth gap is a rolling forecast, continuously balancing core growth (top line and bottom line) with the growth attribution of new initiatives and evolving market conditions.

Step 2: Portfolio Management: From innovation illusion to investor reality

The next step is to create a balanced portfolio of innovation initiatives with the objective of de-risking the uncertain outcome of innovation ROI. There are some indicators about how much growth will be returned from a portfolio of growth initiatives. Alex Ostenwalder looked into the world of VCs to indicate that you need over 100 initiatives in order to get to a specific return. Of course, you can argue about the chances of success and the number of initiatives you need but the key message here is that you need to create a large enough, well-spread portfolio, across a couple of ‘Big Bets’, strategic opportunity areas and protective product extensions. In other words, sticking to the known-knowns will not deliver the revenue growth required.

Portfolio management as fuel for a new approach: from venture building to investment building

According to McGrath, in boardrooms there is a large chance you’ll hear strategic thinking based on ideas and frameworks designed in, and for, a different era. Think about Michael Porter's Five Forces analysis, BCG’s growth matrix, and many others. These are all important ideas but are based on the premise that achieving a sustainable competitive advantage is dependent solely on strategy. We urge a different perspective based on the idea of timely incorporation of competitive advantages (McGrath, 2020). There is a growing gap between traditional approaches to strategy and the REAL world. In order to create a competitive advantage by developing a consistent growth portfolio and product roadmap, we advocate the combination of strategic thinking with an agile iterative “test and learn” approach. This will allow you to uncover early warning signals to validate strategy and timing, identify opportunity areas and co-create with your customers or startups on product MVPs that might stick.

Instead of pushing innovations further after the MVP phase, we push for a more aggressive buy, build, or hold approach. Our quest for validated MVPs allows us to create a focus on discovering a validated concept DNA, based on consumer pains and benefits, product features and early traction. These are the ideal ingredients to either debrief the investor community and scout for ‘ready to invest’ companies or build yourself based on corporate assets. This way of working is all focused on speed and decisiveness to break through the clutter and capture the next (timely) growth wave for your core business. We call this Investment buildingⓒ.

Ultimately, an investment-building approach will make more impact if it solves today's problems and tomorrow’s challenges at the same time. It is the responsibility of senior management to be vocal about these problems and to push for investable innovations to challenge the future. The growth gap north star will push your innovation roadmap to do just this.

Step 3: Growth Governance: Your resource allocation dilemma

According to Clayton Christensen (2003), the resource allocation process needs to be actively managed because resources will follow the path of least resistance. This means that more money will flow to “maintaining the core’ and less towards innovative/ uncertain initiatives that will grow the core (potentially). A couple of steps are needed to create the right balance:

“Consider adding external IC members (an institutional venture investor or a representative of another CVC) who will provide, like independent board members, independent insight without the baggage of internal politics or conflicts,” Professor Strebulaev notes.

Step 4: Investment building

The whole idea of investing in innovation is to create growth for the business, its shareholders and society. We conclude that most of a company’s current activities do not deliver on its growth ambitions, resulting in the shutting down of incubators and labs. The whole notion of investment building is:

To summarize, the goals of the 10x Growth approach are:

- The growth gap is your north star and dictates the content of your innovation portfolio

- Your innovation portfolio is a balance between big bets and sustaining innovation

- Make your time to market manageable with a buy/build/hold approach

- This investment approach benefits the ‘imagination premium of your core assets’.

- Spend your time on understanding the problem, not on building a solution

Step 5: Accelerate with a 10x entrepreneurial mindset

“What lies behind us and what lies before us are tiny matters compared to what lies within us” - Ralph Waldo Emerson

The heart of our model, and what really allows you to accelerate, is an entrepreneurial mindset. Without the right mindset, you won't make the right progress. Innovation, for the core or beyond the core, should remain a colorful, dynamic adventure in which the human/change side needs to be managed proactively in order to avoid irrationality in decision-making. We are not a fan of the macho jargon around “breaking things”, “asking for forgiveness later” and other strongly-worded phrases.

When comparing entrepreneurship within family-owned businesses (FBs) and non-family-owned businesses (NFBs), there is an interesting parallel that can be drawn. Compared to NFBs, FBs score better on long-term vision, are more profitable and more adaptable to change. A study from Credit Suisse shows that stock-noted FBs outperform NFBs by 3-5% annually. The reasoning behind this is that the leadership is personally invested in the company’s success and therefore there is more focus on profit, product growth and ROI at a company level. Another way to look at it is that in NFBs there is less personal attachment, which leaves more room for a mindset focussed on individual gains.

Why is this important? We need to understand that most, if not all, corporate innovators, are always part of a political endeavor. The naivety or unwillingness to accept that this is part of execution is a huge blindspot. As long as the “dark” or “unconscious side” of the change process is not managed proactively, things fall apart, especially with the uncertain outcomes of innovation. The dark and unconscious are often hidden in emotions like love, hate, distrust, uncertainty or simply an excess of passion.

This can’t be managed through an investment deck or memo. Not knowing how to embrace these emotions yourself and instead pushing them away will create irrationality and imprecise interventions. There is no mental capacity for an objective analysis of the situation. We feel strongly about developing capabilities like “reflective action”, “authentic engagement”, “tough love” and other values that bridge opposites (Quinn, 2004). But in reality, these terms describe an ‘and’ not an ‘or’. As successful innovation requires top-down support, similar to the FBs, you as a manager need to create self-knowledge of your unconscious habits of thinking and behaving, so you become more conscious step-by-step and, therefore, a better (innovation) leader.

For us, this is the secret sauce for the 10x Growth OS; the entrepreneurial mindset that puts investment building on the agenda. This is the only route to getting towards an “owner’s mindset” and “consumer obsession”. These values should come from within, not copied from posters or leaders who do the opposite. Let's change innovation for the better! Starting on the inside will lead to winning on the outside.

Chapter summary:

a) Adopt an approach to venture building that connects your existing growth gap with your brand strategies and innovation portfolios.

b)Timing is everything when it comes to innovation, something that can be “manipulated” through combining strategic thinking around early indicators for change with an iterative test & learn approach to test certain assumptions in real market conditions.

c) Corporate venture building remains a great mechanism for corporates to innovate but needs to be executed in a way outcomes fit the dominant way of thinking in the mothership

d) To be successful, corporate venture building should be about learning. Building and acquiring is something the core should do

e) Focus on consumer research to identify the key pain points, then scout and identify the startups that have the functionalities to tackle them. We call this ‘investment building’.

f) Set minimum success criteria for the viability of your ventures and manage realistic expectations.

g) Execute a buy, build or hold strategy for innovation to replace endless MVP building

h) Corporate venture building requires a mindset change from senior management. Be vocal and clear about investment readiness

i) Don’t neglect the sometimes irrational change process of innovation. Prepare your teams to lead in a multi-stakeholder dynamic context

Not for me? Different types of growth

A geographic expansion of an existing product is risky but has fewer unknowns than you get when creating a new product for a new customer segment carrying the same brand logo. But you need both to grow, as existing products have an inherent limit of what they can achieve in terms of sales due to changing consumer needs or competitors entering your market.

Your growth roadmap therefore should represent a counterbalance to all the external factors that eat away at the market share of your product portfolio. This should be owned by the business core, not by a speedboat 10 miles away from the mothership. This is needed to foster the right entrepreneurial mindset, with ownership and strong integration of the roadmap and its initiatives by the business. A clear example of this shift in mindset can be found in Unilever’s statement upon closing The Uncovery. “Since establishing a new Business Group dedicated to beauty, we have decided to reorganize The Uncovery and redeploy the capabilities, learnings and insights back into our Beauty & Wellbeing business, where we continue to drive new business creation and innovate.”

As a corporate, Unilever and others that move in this direction are not necessarily giving up innovation - they are simply bringing it closer to the core. But the core business is, most of the time, (very) profitable, and so starting with new innovation that is focussed on the core by default dilutes the profitability of the business tomorrow. In order to manage these tensions, corporate innovation needs to improve itself with the following elements:

Futuresight

For many corporates, the easiest decisions are those in the near future but anything mid- or long-term that requires innovation is neglected due to uncertainty. This means that we need to be able to better forecast sales trajectories by:

Accounting

This is usually excluded from innovation but most sales and trade marketers struggle to understand the impact of their actions and KPIs or what innovative product concepts perform better than others. As a result, they’re handed new products but are incapable of marketing them. We believe that sales data is your gold mine for branding, as well as the development of new and adjacent products.

Funding strategy

Often, there is enough money to start projects but it becomes difficult to continue funding them once you need to choose between them. It is therefore important to create a funding pool that allows continued investment in projects when they achieve their KPIs. In doing so it allows for a balanced pool of projects that have the security to continue based on value, not sentiment.

The reality in most companies is that innovation is constrained by the system itself. Low-risk projects with close adjacencies to the core are the easy choice. Financial outliers are blocked at stage gates and projects requiring high capital investment or boasting new capabilities face the same fate. This leads to spotting consumer needs and trends but not being able to capitalize on them, which often results in the dilution of an M&A. A change is required:

Chapter summary: Innovation = Learning

More than a lightbulb moment

The competitive gaps of your core portfolio will narrow over time and need to be constantly rejuvenated by innovation, brand and communication investments. Ensure that the KPI set of your core businesses includes an incentive to innovate and grow not only in the short but also medium and long term. This will drive the actions in the right direction and ensure the long-term differentiation and growth of the core portfolio.

As a flywheel for innovation, this is exactly what the 10x Operating System is designed to do.

Do you want to get in touch with us?

We’re here to help. Wether you have a request or a question.

Subscribe to our newsletter